Not long after a bankruptcy is filed the debtor ends up inundated with credit card offers. A common question we receive is “should I get a credit card?” We thought it would be appropriate to address this question at large so you can understand the practical effect and consequences of obtaining a credit card, or any additional debt for that matter, while in a bankruptcy. Many people often say they want to rebuild their credit score. While the topic of this blog is not a discussion of how to rebuild your credit score, it is at least pertinent to understand roughly how your credit score is calculated as it informs the later conversation.

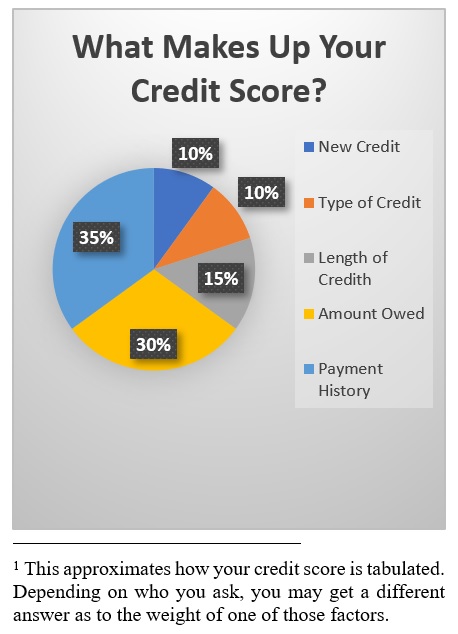

Simply put, your credit score is a numerical representation of 5 factors: New credit accumulation (new lines of credit and inquiries over the last year or so), Type of Credit (installment loans or revolving loans), Length of Credit (how long have you had it) and the two largest factors are the Amount Owed (percentage of credit limits available) and Payment History (whether your payments are on time, delinquent, or past due several months).[1]

“Why is that important?” you may ask. Because those five factors are not treated equally and there is a misconception that obtaining a credit card in bankruptcy will fast track you to rebuilding your credit. By that same token bankruptcy will negatively impact your credit score for a period of seven to ten years depending on chapter. One on-time payment does not an 850-credit score make. All of this is to say, we generally do not advise people to take out credit cards while they are active in bankruptcy. There may be special circumstances which warrant doing so, but those are few and far between.

As a general premise, the bankruptcy court is supposed to authorize any additional debt incurred by a debtor in bankruptcy. In practice many people do not seek court approval for something like a credit card in their Chapter 13. This leads to two interconnected problems. First, the debtor is supposed to commit all their disposable income to fund their bankruptcy plan. If you’re committing all your disposable income to fund your Chapter 13, how can you afford to pay monthly charges on your credit card? Which leads to problem number two, when times get tight you rely on your new credit card then fall behind on paying that. These new debts are not covered by your bankruptcy. It is not hard to see how the new debt can spiral out of control. Speaking of new debt, and by consequence your credit score, someone who seeks court approval for something like a new car will see greater growth to their credit than someone who inappropriately obtains a credit card without approval. This is, in part, because an installment loan is more beneficial to your credit growth than a revolving loan. You may ask “how can I get approval for a car loan if my credit is bad and I’m in bankruptcy?” The answer is, while it may be more difficult for you than someone with an 850-credit score, it is far from impossible. There are lenders who will work with debtors in bankruptcy and understand the additional restrictions they need to meet if they want to complete the sale.

If one were adamant about obtaining a credit card while they are in an active bankruptcy, then the best bet for them would be a secured credit card. Just like the name implies, the secured credit card is secured by a deposit. The deposit protects the issuer from losing money. They tend to be easier for people with poor credit to acquire. Practically speaking, the security deposit you place on the card should provide you with incentive not to miss payments. You want that security deposit back after all.

As debtors’ attorneys we must caution people about acquiring additional debt while in a bankruptcy. Certainly, there are times when the need arises, and a debtor must acquire new debt. Such as the instance we mentioned earlier where a debtor’s car is on its last legs and a reliable mode a transportation is necessary for the case to continue. The debtor should always utilize the proper channels and obtain court approval prior to taking on new debt.

Your credit score will see some natural growth throughout your case. It’s not a thing that will be “fixed” with any degree of haste. The advice we give to our clients is straightforward: do not be so concerned with your credit score, focus on getting through your bankruptcy and making those trustee payments. If you do things correctly you will be free from most debt within the 3 -to-5-year period of your plan, then you can worry about credit score.

The Moral of the Story: While you are in an active bankruptcy your credit score shouldn’t be your primary concern. Whatever reasons caused you to seek bankruptcy protection, the most important thing for you to focus on is being successful and completing your bankruptcy to get the fresh start you needed.